[ad_1]

According to a report by CareEdge, bad loans will continue to drop during the current financial year because of higher credit growth and the transfer of legacy assets to the National Asset Reconstruction Company (NARCL).

Bad loans in the Indian banking system soared after the Reserve Bank of India conducted an asset quality review (AQR) in 2016. The RBI identified loans that were in default but were not recognised, and borrowers were given time. Bad loans peaked at over 10% of all loans in March 2018 and have declined since then following largescale provisioning by banks. Since the RBI conducted the AQR, banks have made over Rs 16 lakh crore provisions.

A separate report by Motilal Oswal said that new defaults would be controlled, which, along with healthy recoveries and upgrades, will result in a continuous improvement in asset quality across banks. It added that while the performance of restructured and government-guaranteed loans would need to be watched, overall credit costs was expected to remain under control, helping banks improve their balance sheet. The brokerage house forecasts a 40% increase in Q1FY23 profit for private banks and a 6% increase for public sector banks.

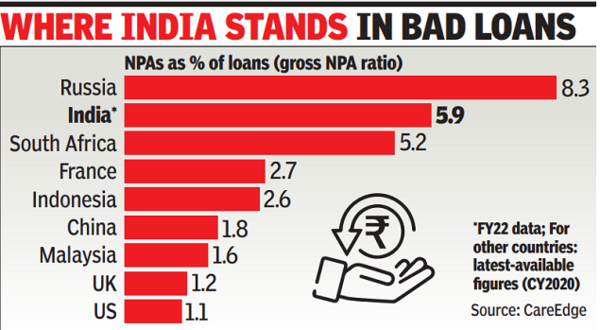

“Despite the continued decline, India’s NPA ratio is one of the highest among the comparable countries. Non-performing loans eased in advanced economies due to continued deleveraging and institutional and government intervention,” said CareEdge.

The RBI has forecast an improvement in the bad loans under a baseline scenario to 5.3% by March 2023 following its stress tests. However, the GNPA ratio may rise under the medium/severe stress scenarios, and the GNPA ratio may rise to 6.2%/ 8.3%, respectively.

In terms of ratio, the gross non-performing assets are highest for agriculture at 9.4%. “Agriculture GNPA generally rose due to droughts and elections – the anticipation of loan waivers,” the CareEdge report said. NPAs for industry stood at 8.4% and services at 5.8%. It continued to be the lowest for retail, dominated by home loans, at 1.8%. Restructuring of loans by entities impacted by the second wave of Covid stood at 1.6% of total advances in December 2021.

[ad_2]

Source link