[ad_1]

Typically, borrowers refinance their home loans to take advantage of lower mortgage rates.

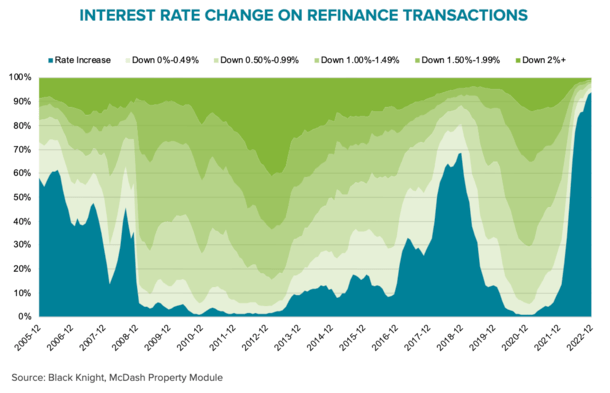

But recently, the average refinance has resulted in an interest rate 2.4% higher than the pre-transaction rate.

Why, it’s mostly because the only homeowners refinancing these days are doing so to tap equity.

The last time we saw a similar phenomenon was in 2018, when almost 70% of refinances involved an interest rate increase.

After that, borrowers saw an average rate increase of 0.4%. What’s up?

Rate and term refinance at all-time low

New one reports Black Knight revealed that of the 216,000 mortgage refinances completed in the fourth quarter of 2022, 96% were cash-out loans, the highest quarterly share on record.

Meanwhile, there were less than 10,000 rate and term refinances, the lowest on record.

Prior to Q4 2022, the lowest quarterly total was 76,000 in 2018. The average 15 years ago has been 650,000 per quarter.

And in the first quarter of 2021 alone, there were 1.8 million rate/term refs, 190 times the total for the fourth quarter of 2022.

For all of 2022, 1.98 million cash out refinances were completed, accounting for over 80% of all refinances for the year.

In other words, the refinancing market has been dominated by cash refinancing, which is completely understandable.

With mortgage rates hovering around 7%, there’s little reason to refinance unless you’re tapping home equity.

The only other reason, other than removing someone from an existing loan, would be to switch from an adjustable-rate mortgage to a fixed-rate loan.

But those situations appeared to be few and far between.

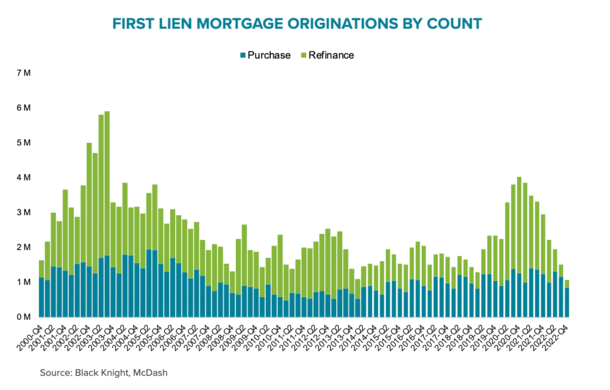

The 216,000 refinances in Q4 2022 (including 62K in December) were also an all-time low.

And the 863,000 purchase mortgage originations were the lowest since 2015, pushing overall quarterly mortgage volume to its lowest point on record (dating back to 2000).

Average mortgage refinance caused interest rate to be 2.4% higher

Black Knight noted that cash-out refinance volumes have also declined of late, but “should also make up the lion’s share of refinanced loans in early 2023.”

Which is pretty wild, 94% of those who refinanced this past December raised their interest rate in the process.

And the typical refinance resulted in a 2.4 percent increase in borrowers’ interest rates!

For example, a borrower may have a rate of 3.5% before refinancing, and now has a rate of 5.875%.

Of course, if they need cash, they need cash. And while an interest rate of around 6% isn’t as favorable as 3.5%, it probably beats the rates on all other types of loans.

So the cash-out proceeds can still be used to pay down other loans, possibly with much higher interest rates, in the double digits.

For perspective, the average borrower who refinances in early 2021 receives an average mortgage rate reduction of 1.3%.

As seen in the chart above, mortgage rate increases were also common after refinancings in 2005-2008.

After that, there were also a lot of cash out refinances. And borrowers were often refinancing successively to cover discretionary purchases.

Lowest quarterly cash out volume since 2015

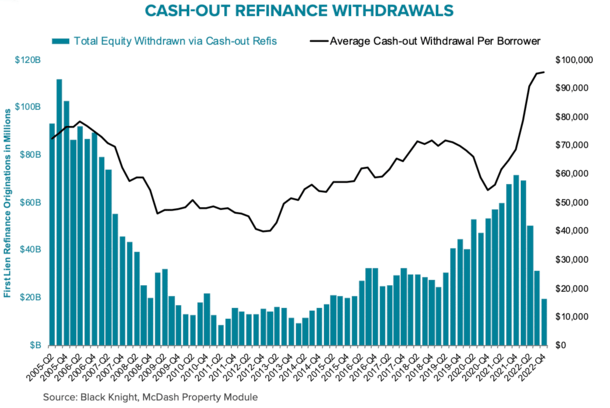

Despite leading cash out refiles, just $19 billion of equity was withdrawn during the fourth quarter, the lowest since the beginning of 2015.

And cash-out withdrawals amounted to just 0.2% of eligible equity in the quarter, the lowest on record.

In other words, there’s a ton of home equity out there that’s been left unused.

This is in stark contrast to 2006-2008, when homeowners tapped every possible penny through 100% CLTV cash out refinances.

However, the average amount of equity increased from less than $55,000 in late 2020 to more than $95,000 recently.

That’s why those who are withdrawing cash are withdrawing more money.

But the average unpaid balance (pre-equity extraction) of these borrowers declined from nearly $240,000 at the beginning of 2020 to $165,000 in the fourth quarter.

This means that people with small existing home loan balances who need a lot of cash go the cash out refinance route,

Meanwhile, those with large existing home loan balances are opting to retain their low mortgage rates and tap equity through second mortgages.

By choosing to take out equity through a home equity loan or HELOC, they can hold onto their low, fixed-rate mortgage for years to come.

As for increases in mortgage rates for homeowners, they could benefit from refinancing in the near future if the rate trend falls back to 4-5%.

[ad_2]

Source link