[ad_1]

Mortgage rates fell nicely to start the week but only after a sharp increase in the previous two weeks. That said, short-term fluctuations are just a sideshow in the bigger picture where rates are locked in a pattern of indecision that will eventually give way to the next big move.

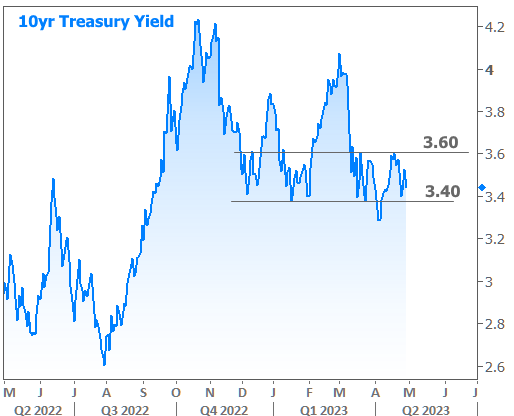

There is a slightly smaller version of the bigger picture seen in 10yr Treasury yields, which are highly correlated with mortgages.

If it seems like Treasuries are a bit more willing to hover near the bottom of their range, there’s good reason for that. A resurgence of concerns over the banking sector sent investors seeking refuge in the safest places. After several back-and-forth headlines, the week ended with reports that it was only a matter of time before First Republic Bank officially failed.

In not so many words, when these banks officially fail, another bank or financial firm acts as trustee to reduce the amount of the FDIC’s insurance payments. It involves selling the assets of the bank. In SVB’s case, there are billions in mortgage-backed securities. From there, it’s just supply/demand 101. Higher supply = lower prices. And in the bond market, lower prices mean higher rates.

What will it take to change things? In a word: Inflation. After all, that’s how we got here in the first place. The current market is a reflection of current inflation in the balance sheet, which has been more stable than many fans of low rates would expect.

This week brought another update on the inflation situation in March, this time from the PCE price index (not to be confused with the Consumer Price Index or CPI which has a much greater influence on rates). PCE prices were near expectations, but did not seem eager to return to the target level.

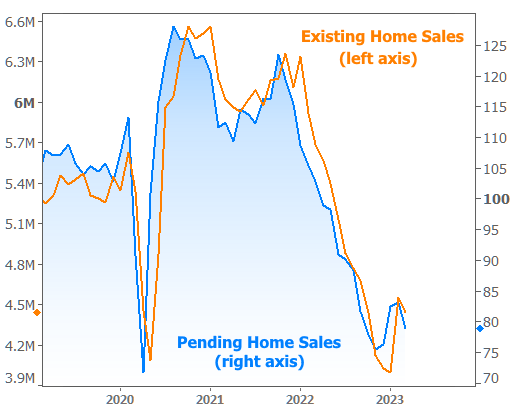

In separate data, some of the effects of March’s higher mortgage rates were seen in the form of fewer pending home sales. This data series is a leading indicator of current home sales for the National Association of Realtors. The chart below compares the two. Simply put, the sharp drop in pending sales suggests that the housing market is also in a limbo of sorts and is not necessarily looking forward to a sharp rebound.

Next week brings more important economic data as well as the latest rate decision from the Fed. It is almost certain that we will see another 0.25% rate hike, but at that point, an even closer look at the data will take place to determine if there is a ceiling until further notice.

Next Friday’s jobs report and next Wednesday’s release of consumer price index rates could go a long way toward challenging the sideways pattern, but only if they both send the same message.

[ad_2]

Source link