[ad_1]

Scroll down far enough on Webster’s list of definitions of the word “consolidate” and you’ll find “to form together into a compact mass.” Financial markets appropriated that definition long ago and it has been used to refer to the condensed mass of prices, yields, or whatever is being measured on a chart.

Speaking of charts, consolidation consists of a tell-tale pattern of lower highs and higher lows that form a triangle or pennant of sorts (incidentally, market participants also use those terms more or less interchangeably).

Regardless of the label, the underlying phenomenon is one of indecision or anticipation of a larger move that has a chance to go higher or lower.

Consolidation is ruling the market these days. If we zoom out and just consider the general flow of events, it makes good sense. As inflation rose at its fastest pace in decades, the Fed tightened monetary policy at an equally fast pace. Inflation can also act as a natural brake on economic activity as consumer purchasing power declines.

At some point, the level of inflation growth levels off and we wait for a return to more sustainable levels of price growth. The presence of consolidation is understandable because we’re smack dab in the middle of figuring out whether inflation has leveled off as a sign that it’s about to ease, or simply needs to take a breather before remaining stubbornly high. For. Consolidation patterns are equally likely to be observed for both reasons.

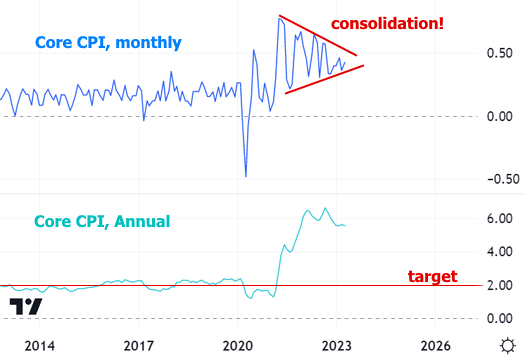

The focal point and broad consolidation theme for economic data this week was the release of the Consumer Price Index (CPI) for April on Wednesday. More than any other inflation report, the CPI has the power to move rates higher or lower faster.

The CPI was in line with expectations this time, which doesn’t really help dispel much indecision. The 0.4% monthly change at the core level (which gets most of the attention from the Fed and financial markets) is right in the middle of a consolidation pattern. And the annual number has remained fairly flat, down from the highs seen in late 2022.

There were some subtleties under the headlines that were helpful for rates. Notably, there was a substantial deceleration in inflation in core services, excluding housing. This is a hot button for the Fed, as it captures the vast majority of the inflation that has been most problematic. Removing housing from the equation allows the market to see a change earlier than it would otherwise (because the housing component doesn’t move as much or as quickly).

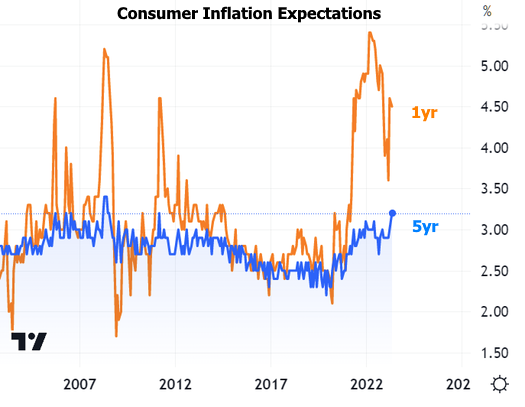

Suffice it to say: Interest rates went lower on Wednesday despite CPI coming in flat. The next day, unemployment claims and the producer price index (PPI) helped the move continue, although bank sector drama also kept investors from the U.S. Yields jumped on Friday after a consumer sentiment survey showed 5-year inflation expectations at their highest since 2011.

The 10yr Treasury yield chart above is a good proxy for interest rate movement throughout the week. This may not sound like a good example of consolidation on such a short time scale, but if we zoom out, things change.

And what would be a good proxy for rate momentum if its sideways vibes don’t translate to the mortgage market?

In fact, as of Friday, mortgage rates saw their flattest calendar month since May 9 through June 9, 2022.

The point of all this consolidation observation is simply to suggest that the market is at a crossroads – albeit with a very long stop light – that will inform the next big move for rates and the housing market.

If inflation eases out of its consolidation pattern, rates will almost certainly do the same, thus giving homeowners some breathing room for new homes without having to worry about giving up their extremely low current rates. Is.

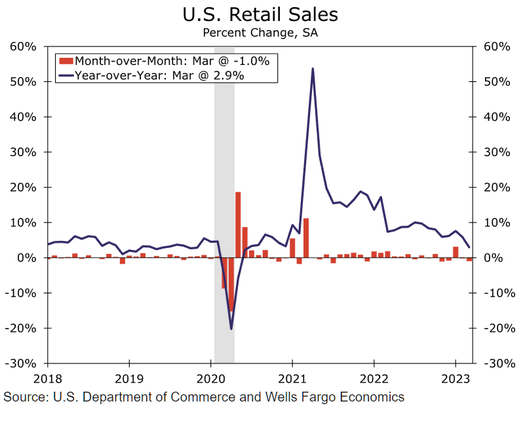

In the coming week, we’ll get to see how that process plays out through Thursday’s current home sales data. Two days ago, the retail sales report will provide an update on consumer spending. In general, lower sales indicate easing pressure on inflation, but economists expect an increase of +0.7% this time, compared to a decrease of 0.6% in the last report.

[ad_2]

Source link