[ad_1]

Rates may not be as high as they were several months ago or as low as they were 5 weeks ago, but they are close enough to either threshold that the threat (or promise) of a comeback is clear. For the last 2 weeks at least, we were waiting for this week’s events to give us some kind of push or less, but it looks like the wait will continue.

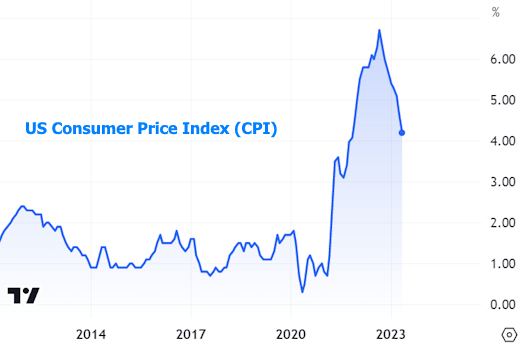

The two major events in question were the release of the Consumer Price Index (CPI) on Tuesday and the Fed announcement on Wednesday. The CPI is the most widely followed inflation metric among regularly scheduled economic reports. It comes once a month and has had a huge impact on rates several times in the last 2 years. This time, it happened to come the day before a particularly important Fed policy announcement.

The year-over-year CPI was set to continue declining in this week’s report because it was so high 13 months ago (i.e. this is a 12-month count and there was no way the current month was going to be as bad as the month it was right now). has been bumped) out of the equation).

The month-by-month numbers filter out the effects of the past and show more detail. This is where we see the first impasse that remained unresolved this week. Simply put, month-on-month inflation remained entirely within the bullish narrow lateral range that it has sustained for nearly 2 years. This provided valuable guidance for the Fed announcement the next day.

Most of the market expected the Fed to hold its policy rate steady at this meeting. The “policy rate” refers to the fed funds rate that applies to overnight lending among large financial institutions – something that changes no more than once every 6 weeks and unless the Fed actually hikes/cuts.

Longer-term rates (such as for mortgages) are of more interest in the forward-looking trajectory of the Fed’s rate path. At every other meeting, the Fed releases a summary of economic projections. A crowd favorite is “The Dots”—a reference to the dot plot that shows each Fed member’s perceptions of where policy rates will be in the near future.

This example of the dots was particularly interesting because it would provide insight into whether the Fed was actually holding off on a rate hike or if it thought it might have reached the ceiling. On that subject, the DOTS left little to the imagination, with the average vote apparently moving 0.50% higher, thus leading to 2 more rate hikes in 2023. All this without any strong guidance from the CPI data. One can imagine that the points could have been higher if CPI had been hotter.

Markets were initially unhappy to see the Fed tilt toward even tighter policy, but found solace at a press conference with Fed Chair Powell. In it, he offered his characteristic reminder that the dots are just estimates and not predictions or forecasts (whatever that means). If he could speak more clearly, he would probably say something like “The dots are just an approximation of how things look today. We force these people to pick a number. Most pick wrong. And so on. Depending on how the economy turns out, most will change their forecast in 12 weeks when the next points come out.”

Powell further said that the Fed had not even decided whether it would raise rates again. It will be taking decisions on a meeting basis based on the evolution of the data. To say that economic reports are over-emphasized would be an understatement. With some showing strength and others promising bearishness, it’s no surprise that a volatile, sideways range remains intact.

In the case of the 10-year yield, the short-term sideways range is probably too narrow to last very long, but it has offered solid guideposts recently.

In the bigger picture, the border isn’t entirely sideways. It is more than fighting to get back down to the 3.4% level.

As always, trends in 10yr yields largely reflect trends in mortgage rates.

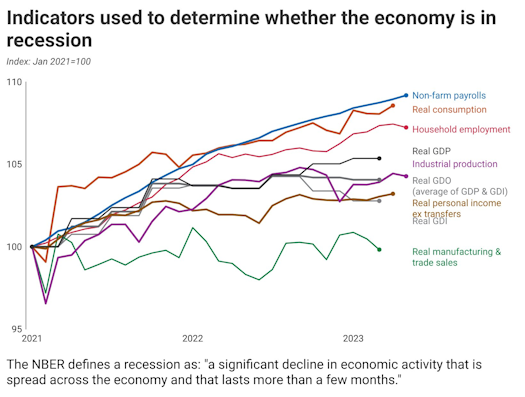

So what does the data say about how things might develop in the near future? Seriously, it’s up for debate! The following chart from economist Justin Wolfers made the rounds on Friday, silently lamenting that it’s ridiculous to expect a recession right now based on most economic data.

Around the same time, economists at Wells Fargo released their weekly note with some thoughts on recent trends in the Leading Economic Indicators index ahead of next week’s update:

“In a world full of backward-looking economic data, forward-looking indicators such as the Leading Economic Index (LEI) are certainly valuable. Unfortunately, the LEI has been fairly consistent in its indication of recession. The six-month average change of the threshold for this index has consistently With declines for 10 months down to historically recorded lows. The downdraft of LEI is also gaining momentum, suggesting that the potential for a business cycle turnaround is high.”

It’s all too easy to sway the debate back and forth between “recession” and “it’s not so bad” with other data this week. While we’re on the subject of sentiment surveys, how about consumer sentiment? It may be historically low, but it is also trending fairly consistently higher (in complete opposition to the trend seen in the above chart).

On a more bearish note, weekly jobless claims have touched their highest since 2021 for two consecutive weeks.

And if we filter out the noise associated with the pandemic, these are actually the highest levels since 2017.

As long as there are compelling ways to make a case for the opposite economic outcome, it will be easy for rates to remain roughly sideways, but with large, volatile swings between prevailing highs and lows. It’s a waiting game for now.

[ad_2]

Source link