[ad_1]

Apple will now let consumers use its mobile payment service, Apply Pay, to make purchases immediately and pay for them in installments over time.

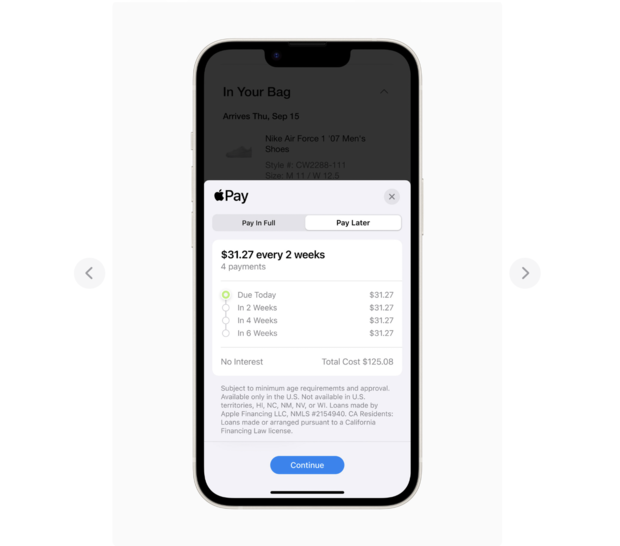

With “Apple Pay Later,” users have the option of splitting purchases into four payments made over six weeks. They will not be charged any interest or fees, the company said in a statement on Tuesday announcing the new feature. Users also can apply for “buy now pay later” loans of $50 to $1,000, made through Apple Financing, that can be used for online and in-app purchases at any vendor that accepts Apple Pay.

Currently, “Apply Pay Later” is only available to a select group of users. The company plans to roll out the feature more widely in the coming months, Apple said.

Apple

More than 40% of Americans have used “buy now, pay later” services, according to a Lending Tree survey.

Although Apple touts the feature as one that was designed with “users’ financial health in mind,” research has showed that many Americans struggle with buy now, pay later loans, which have become more popular along with the surge in inflation.

The loans are designed to encourage consumers to spend and borrow more, and users are subject to fees if they miss payments, which can lead to their accumulating more debt.

In 2021, buy now, pay later loans totaled $24 billion, up from $2 billion in 2019, according to a CFPB report. The payment option has become ubiquitous in stores and online, forcing regulators to play catch up. At the same time, the agency has seen a steady rise in the percentage of borrowers who fall behind.

Thanks for reading CBS NEWS.

Create your free account or log in

for more features.

[ad_2]

Source link

(This article is generated through the syndicated feed sources, Financetin neither support nor own any part of this article)