[ad_1]

The California Housing Finance Agency has launched a new shared appreciation loan for home buyers.

The program, known as the “Dream for All Shared Appreciation Loan,” allows Californians to build wealth through home ownership without a down payment.

In lieu of that down payment, they have to share a portion of the future appreciation of their home.

While this can be a costly compromise, it eliminates the need for a significant amount of money at closing.

And by avoiding a large loan amount or second mortgage, buying a home can remain affordable.

How the Dream for All Shared Appreciation Loan Works

In short, home buyers in the state of California can get their hands on a zero down mortgage, but they must be trading up a portion of future home price increases.

So if a potential buyer doesn’t have a 20% down payment (or a 5% down payment), they can take out a shared appreciation loan instead.

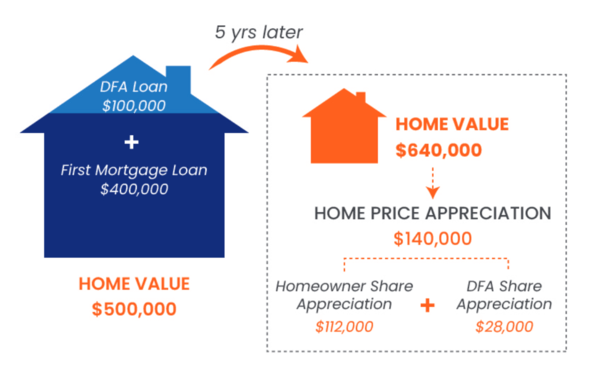

For example, if the purchase price was $500,000 they could get a $400,000 first mortgage at 80% loan-to-value (LTV).

Then CalHFA Will provide a $100,000 DFA (Dream for All) loan that requires no monthly payments.

Instead, the shared appreciation loan is repaid only when the property is sold or transferred, or the mortgage is refinanced.

As a result, the homeowner will have a smaller loan amount ($400,000) and the borrower will avoid costly private mortgage insurance.

Shared Appreciation Loan vs 3% Down Payment

| $500,000 home purchase | 3% down payment | 20% Down w/ DFA Loan |

| loan amount | $485,000 | $400,000 |

| mortgage rate | 6.5% | 6% |

| Monthly P&I | $3,065.53 | $2,398.20 |

| mortgage insurance | $226 | Not Applicable |

| Total | $3,291.53 | $2,398.20 |

While other solutions exist that require only a 3% down payment, the monthly cost can still be very high.

This is driven by both mandatory mortgage insurance for LTVs above 80% as well as higher loan amounts at 97% LTVs.

Simultaneously, borrowers face higher housing expenses each month, potentially putting homeownership out of reach.

The table above is an example I obtained on a hypothetical $500,000 home purchase.

As you can see, a 3% down payment results in a monthly mortgage payment of $3,291.53.

Meanwhile, the 20% down mortgage combined with the shared appreciation loan results in monthly payments of only $2,398.20.

This is due to high mortgage rates at 97% LTV, a large loan amount and monthly private mortgage insurance (PMI).

This can make the purchase of a home unaffordable for a low or moderate income home buyer.

*The effective interest rate on the DFA is equal to the average annual growth of the home during the time it is held.

How Much Future Appreciation Is Shared?

As mentioned, the home buyer does not have to make payments on the shared appreciation loan.

But upon sale, transfer, or refinancing, they must pay off the loan and part with a percentage of the appreciation.

Borrowers with income above 80% area median income (AMI) are subject to 1:1 appreciation share.

For example, if you borrow 20% through the Shared Appreciation Loan and the home increases in value by $140,000, 20% ($28,000) of that total will go back to CalHFA.

Borrowers with income less than or equal to 80% AMI get a lower 0.75:1 appreciation share.

So those who borrow 20% will only share 15% of future price appreciation, or $21,000 in their example.

Dream for All Shared Appreciation Loan Requirements

- First time home buyer and must have complete education

- Property must be a one-unit owner-occupied home or condo

- Income limit based on CalHFA income limit up to 150% AMI

- Dream for all should be combined with traditional first mortgage

- Minimum CLTV is 70%

- Max CLTV is 105%

- Shared appreciation loan amount up to 20% of the sale price or appraised value

To qualify for the Dream for All Shared Appreciation Loan, borrowers need to be first-time home buyers.

This generally means that one has not owned and occupied their property in the last three years.

Additionally, two levels of homebuyer education counseling must be completed and the borrower must obtain a certificate of completion through a qualified counseling organization.

Property must be a single-family residence (1-unit only) or an approved condominium/PUD. Manufactured housing is also permitted.

And it must be owner-occupied (not a second home or investment property) and non-resident co-borrowers are not allowed.

Finally, it should be used in conjunction with the Dream for All traditional first mortgage.

Are Shared Appreciation Loans Bad For The Housing Market?

While shared appreciation can boost loan affordability, they can have the unintended consequence of increasing home prices.

If buyers really can’t qualify for mortgages without massive help, it could mean there’s an imbalance in the market.

The absence of such favorable programs may force prices to drop to better align area incomes with area home prices.

But we’ll never know if this kind of creative financing continues to surface, keeping demand high regardless of price.

This special program aims to increase wealth for low and moderate income earners, as home equity is a key driver of wealth.

However, what happens if home prices do not appreciate like in this example?

Perhaps buying a cheaper house and getting the full amount of appreciation is a better way to proceed.

Regardless, with home prices still far ahead of incomes, such programs will continue.

Read more: Unison will provide half your down payment in exchange for future appreciation

[ad_2]

Source link