[ad_1]

When it comes to buying a home, many people have pondered the buy now or buy later question.

Waiters are waiting for home prices to drop, knowing that affordability is historically low.

Non-waiters either can’t wait or don’t want to wait because they expect competition to heat up once things change. Or they shopped without knowing that prices had peaked.

But is it possible to get the best of both worlds? Can you buy a home at a lower rate and refinance at a lower rate later?

Let’s do the math to see how this would pan out.

who didn’t wait to buy a house

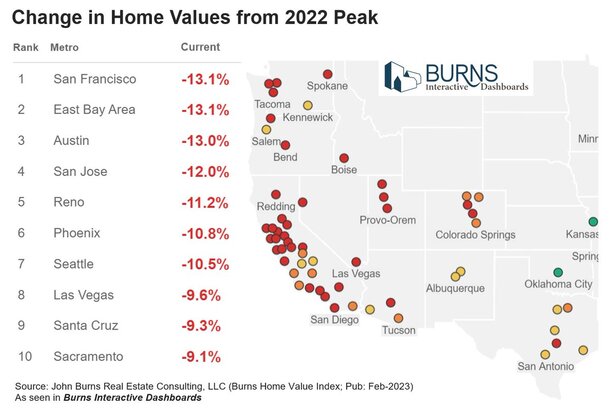

I’m going to be using the Austin, Texas metro for this exercise. prices are apparently down about 13% from their 2022 peak.

Let’s say someone bought a house during there “peak” for $600,000 and put 20% down.

This is a $120,000 down payment and a loan amount of $480,000. We will assume that he has got a 30 year fixed deposit at 3.75%.

The monthly principal and interest payment is $2,222.95. Too little down payment, but they go on Redfin/Zillow and find that their property is now worth about $525,000. Ouch.

Thanks to their 20% down payment, they are not in a negative equity position. But his LTV is now over 90%, at least on paper.

They’re basically going nowhere, but they have a 3.75% fixed-rate mortgage for the next three decades.

Those who waited to buy but missed out on mortgage rate lows

Now consider a buyer’s market entry in February 2023 with home prices down by about 13%.

That $600,000 home is now priced to sell for around $525,000. That means a 20% down payment sets them back $105,000. And the loan amount at 80% LTV is $420,000.

Good news on low down payment and low loan amount. However, the 30-year definitive climbed much higher to 6.5%.

This results in a P&I payment of $2,654.69 per month, which is $431 more than someone paying $75,000 more for the same original home.

If the loan is held to maturity, we’re talking about $536,000 in total interest paid.

The 3.75% loan would result in a total interest of only $320,000.

This does not bode well for the home buyer, who has been waiting for prices to come down given the steep rise in mortgage rates.

But what if rates stabilize again by the end of 2023?

Recent Home Buyers Who Refinance Their Mortgage

| $600,000 purchase | $525,000 Purchase | $525,000 Refinance | |

| Down payment (20%) | $120,000 | $105,000 | Not Applicable |

| loan amount | $480,000 | $420,000 | $420,000 |

| mortgage rate | 3.75% | 6.5% | 4.5% |

| Monthly P&I | $2,222.95 | $2,654.69 | $2,128.08 |

| interest paid | $320,262.00 | $535,688.40 | $346,108.80 |

| complete payment | $800,262.00 | $955,688.40 | $766,108.80 |

Let’s imagine a scenario where inflation gets under control, the Fed stops raising rates, and long-term mortgage rates ease.

No, not back to 3%, but let’s say 4.5%. The buyer takes advantage of this and lowers his rate to 4.5% through rate and term refinancing.

The monthly payment drops to $2,128.08, about $100 less than the person who bought at the “peak”.

And the total amount paid over the life of the loan is approximately $766,000 versus approximately $800,000 on the loan taken out at peak.

Recent buyers still pay slightly higher interest, but less overall due to the smaller amount borrowed.

Of course, this only works if mortgage rates drop substantially from the 6% range to the 4% range. It’s certainly possible, but not guaranteed.

And meanwhile the monthly payment is an extra $400+. TIC Toc.

Still, buyers with higher mortgage rates have options, while buyers with below-market rates can’t really improve their situation.

Another benefit to a lower sales price is a better tax base, and potentially less competition from other buyers if higher rates reduce demand.

The downside is that you will have to go through the stress and aggravation of the home loan process twice.

And as mentioned, there’s no guarantee mortgage rates will actually come down.

But that’s the basic premise of marrying home, date the rate line you’ve crossed.

[ad_2]

Source link