[ad_1]

March was a tough month for home prices.

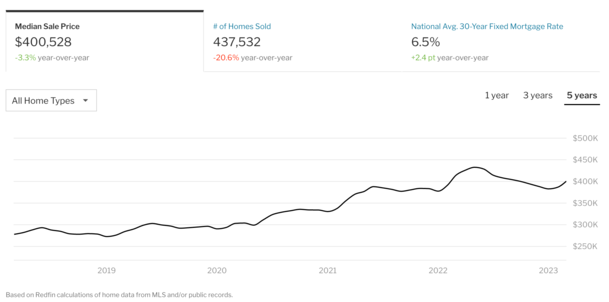

The median US home price fell 3.3% to $400,528 in March, the biggest year-over-year decrease in more than a decade.

This was on top of a 1.2% drop in February, which was the first annual drop in prices since 2012, according to Redfin.

At the same time, pending home sales fell to their lowest level since the start of the COVID-19 pandemic.

And while supply remains an issue, there is also a dearth of buyers due to very high mortgage rates.

Home price drop worst since bottom of mortgage crisis

Home prices were projected to decline by 3.3% from March 2022 to March 2023, the worst annual performance since 2012. redfin,

The average price has also declined by 3.6% month-on-month since February.

If you recall, home prices plummeted in 2012 following the Global Financial Crisis (GFC), which destroyed property values in the previous years.

At the time, the decline in home prices was caused by subprime mortgages and declared income underwriting.

Today, the decline may simply be a symptom of declining potency. This is an important distinction because it can decide what happens next.

Most pundits have blamed the recent reversal in home prices on affordability, with the popular 30-year average fixed rate the main culprit.

It has soared from a high-2% range to nearly 7% in a span of 12 months, wreaking havoc on the pocketbooks of potential buyers.

But if you ignore that piece, there is still strong demand from buyers. And also very high demand in some markets.

This makes today’s housing market very different from the climate of 2006-2008.

Home prices remain 32% higher than pre-pandemic levels

Despite the worst 3.3% drop in a decade, home prices remain well above recent levels.

The median sale price of a US home in March 2020 was $303,059, according to Redfin statistics, It was about that time when we all were locked down due to the pandemic.

Fast forward to today and the average price is $400,528, an increase of almost 32%. So while the title may be shocking, you have to keep it in perspective.

Warning are the so-called “pandemic boomtowns” and the Bay Area, which have seen significantly larger declines.

Prices in Boise, Idaho, were down a whopping 15.4% from a year ago, the worst performer in Redfin’s analysis.

Other big losers include Austin, TX (-13.7%), Sacramento, CA (-11.9%), San Jose, CA (-10.5%), and Oakland, CA (-9.7%).

However, as you can see from the chart above, national house prices are already high.

So some of the upcoming data may indicate a strong start to 2022 before mortgage rates rise.

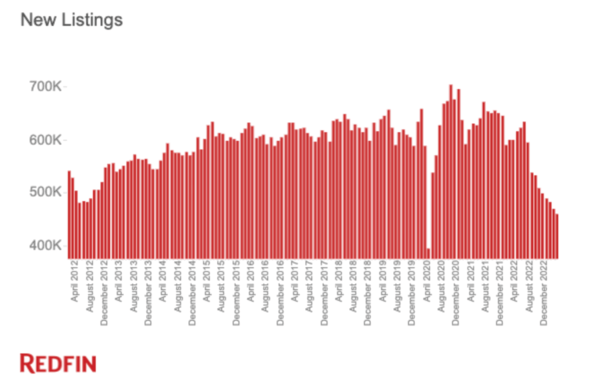

New listings are down 23.3% from a year ago

What makes today’s housing market different from the one seen during the Great Recession is the lack of inventory.

In fact, new listings were down a whopping 23.3% in March from a year earlier, from the lowest level on record (besides the start of the pandemic).

This dearth of homes available for sale has resulted in an even bigger 26.6% drop in pending home sales.

The number of homes sold in March 2023 was also down 22.3% compared to a year ago.

However, active listings are up 5.6% from a year ago, thanks to 23 more days on the market, pushing the months supply in March 2022 from 1.2 to 1.9.

In terms of how homes are performing in today’s market, 44.3% faced competition (multiple bids) and 28.5% sold above their list price.

Both of these metrics are down year-over-year, but given the sharp increase in mortgage rates, things could be much worse.

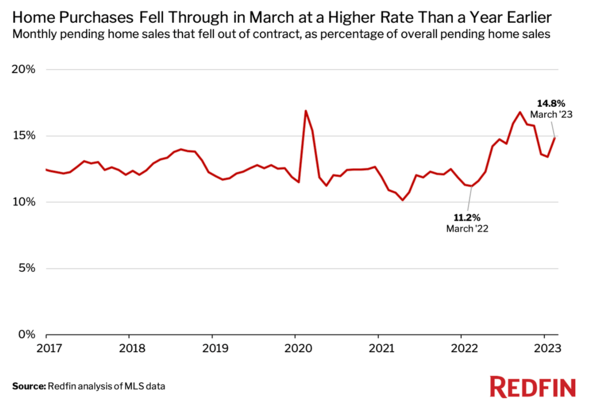

Home purchases are declining at a high rate

Meanwhile, more home buying has come down in recent days.

Some 55,000 home-purchase agreements were canceled in the month of March, accounting for 14.8% of homes that went under contract.

While that number is down from the 2022 peak of 16.8% (when mortgage rates exceed 7%), it is up from 11.2% a year ago.

Interestingly, it is not just home buyers getting cold feet. Redfin cited one home seller who received multiple bids but then pulled the listing.

Why? Because his own mortgage rate was about to double when he moved in. This is the mortgage rate lock-in effect you’ve probably heard about.

The current owners aren’t looking to replace their low, fixed 2-3% mortgage rate with a new one set at 6%.

And that probably isn’t going to change anytime soon unless mortgage rates make a meaningful move back to the high -4% levels.

Don’t pin your hopes on him.

[ad_2]

Source link