[ad_1]

Budget day is around the corner, with Finance Minister Nirmala Sitharaman presenting budget 2023 on 1 February 2023. It’s one of the most important days of the year for the Indian markets and traders prepare themselves for extreme volatility and erratic moves in all exchange-traded asset classes.

In today’s time, most of the market participants are trading in the equity futures and options segment which makes it essential for them to understand the behavior of volatility, both pre and post-budget, especially for options trading. If you are planning to trade the derivatives market on the budget day, then here’s a glimpse of how the has reacted one month before, after, and on budget day in the last 13 years.

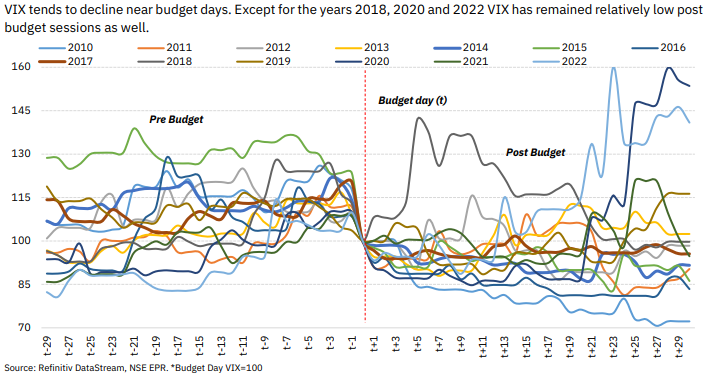

Image Description: Movement of India VIX pre & post-budget, with budget day VIX rebased to 100.

Image Source: Refinitiv DataStream, NSE

Talking about the volatility, it can be clearly seen that the India VIX (which depicts the volatility of the index) tends to remain almost rangebound prior to the budget, but with a slight uptick in the second half of January (t+15 onwards). However, during the entire lookback period, all 13 years witnessed a volatility decline on budget day, which is an expected move.

Volatility generally tends to rise prior to an event on account of uncertainty and falls immediately after the event materializes, as uncertainty gets out of the way. Keeping 2018 aside wherein the volatility spiked immediately after the budget and 2020 & 2022 which also witnessed a post-budget volatility spurt, all remaining 10 years in the last 13 saw a downtick in India VIX over a few days after the budget.

This data is especially helpful for options traders. Options pricing constitutes a few greeks and volatility, also known as vega is one of them. Whenever there is an uncertain event coming up, vega increases which further leads to inflated options prices, making them more expensive. This volatility increase can also be seen in the above chart. Hence, buying options prior to the budget might not be a good idea if the index remains more or less stagnant as post-budget volatility crush would put a serious dent in the options price.

Even if the trader is able to gauge the right direction, still it is difficult to get enough of the delta to counter vega. In other words, the movement of the Nifty 50 should be of considerable magnitude to make a profit on the long option position to outpace the negative effect of a fall in vega (volatility). And in case the Nifty 50 gives a one-sided move in the opposite direction of your position, then the loss is almost difficult to cope with as both the delta (direction) and vega would slash the options price.

So is it appropriate to short-sell options? Well, from the volatility perspective, the answer is yes. In my experience, even if the index moves in the wrong direction (w.r.t your position) you still get enough time to make an exit as the volatility crush comes to your rescue (to some extent). If the index remains sideways without any fireworks, that can easily take your positions to the green. And, if you pick the right direction, then that’s a jackpot! Selling options prior to the budget also means you can get higher prices which further increases the magnitude of potential profits.

I might seem biased toward short-selling options prior to the budget, but that’s my way of trading the budget day. You can definitely have your own way to go about it as there’s no one-stop solution to trading.

Tip: Whatever you do (options buying/selling) going into an event day with a hedged position is always recommended.

[ad_2]

Source link

(This article is generated through the syndicated feed sources, Financetin doesn’t own any part of this article)