[ad_1]

The first week of a given month has the highest concentration of economic data with the power to influence the bond market, and thus interest rates. This week was no exception.

Apart from the scheduled economic data, there was unscheduled drama in the banking sector as well. This included the systematic failure of First Republic Bank, rumors of other impending bank failures, and a run on various bank stocks that eventually required several “circuit breakers” (temporary interruptions of business due to the size and speed of price changes). .

Bank drama followed on Tuesday morning with fewer jobs to send bond yields lower on Tuesday. This was easier to see in the 2yr Treasury yield than the 10yr Treasury, which we usually follow because shorter duration bonds are more common with the fed funds rate.

A day later, we heard from the Fed itself about the widely anticipated 0.25% increase in the fed funds rate. Despite the hike, interest rates remained broadly low mid-week (Mortgage Rates in the Weeks After the Fed Hiked Rates. How It Works…” data-contentid=”6452c40c9d238671bb2d6f63″ data-linktype=”rateupdate ” rel=”noopener”>Here’s why) before pouncing after Friday’s strong jobs report.

All told, the 10-year yield traded in a range of about 0.25% while the 2-year yield saw a range closer to 0.50%. It’s a volatile week by any standard, but it’s still failed to blaze any new marks with respect to the range we’ve been following in 10yrs. One could argue that yields were pushing the lower limit of the range were it not for NFP (“non-farm payrolls,” the main component of the jobs report) on Friday.

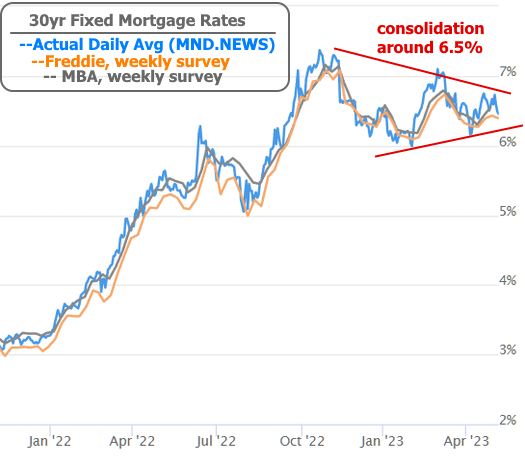

Mortgage rates haven’t necessarily been keeping pace with Treasuries, but they’ve been equally sideways. In fact, rates are consolidating in a narrowing pattern around a traditional 30yr fixed rate of 6.5%.

While this week’s volatility was well distributed across multiple days and events, next week’s potential volatility is highly concentrated on Wednesday morning. Only then will the latest monthly installment of the Consumer Price Index (CPI) be released.

CPI is the biggest market mover among the various inflation reports that come out every month. This is the only report that can legitimately challenge NFP as the most important monthly data in the past few years. Every new update on inflation is especially interesting right now because the market is actively trying to determine whether inflation is under control and declining, or if it’s persistent enough to require more rate hikes from the Fed. . This indecision is about a consolidation pattern in mortgage rates.

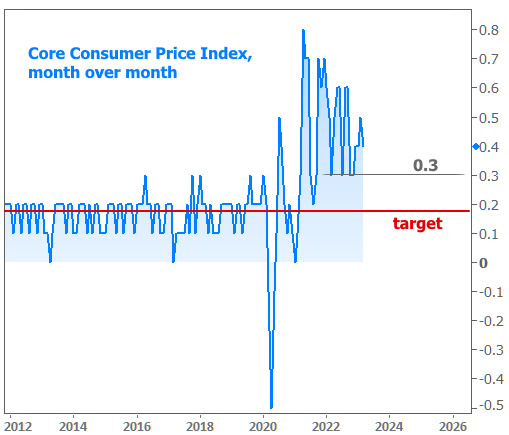

The most important figure in the CPI data is the monthly “core” reading that excludes the more volatile, less elastic food and energy prices. It topped out at 0.8% at the highest level and though it has come down slightly, it is still well above the target range.

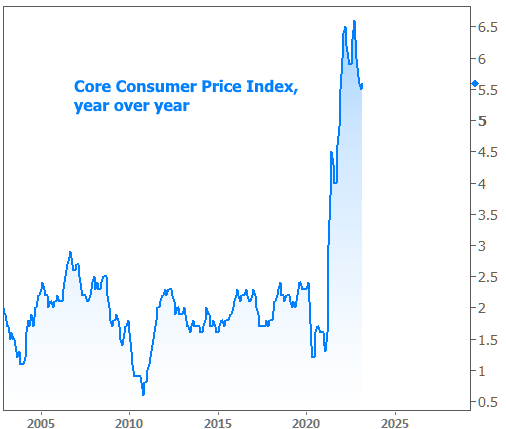

Achieving the 2% target of 0.167% core inflation will take 12 months. Obviously, there’s a long way to go, but if the market is convinced that we’re headed in that direction, rates will be much lower than they are now. The year-on-year chart is still anything but reassuring.

[ad_2]

Source link