[ad_1]

“Market timing can appear to be a fool’s game. But that’s only half the story.”

The S&P 500

SPX

would be up more than 30% this year as of November 8, but for eight particularly bad days for the U.S. market. That’s more than double the benchmark index’s actual return of 14.1% over that time.

I point this out to provide additional perspective on a provocative report from DataTrek Research, which recently reported that the S&P 500’s return through Nov. 8 was due primarily to the year’s eight best trading days.

This is important because if you focus only on what happens when you miss the best trading days, market timing can appear to be a fool’s game. But that’s only half the story. A defender of market timing could just as easily focus on the huge benefits that accrue to sidestepping the biggest losing days.

“What if you had equal success avoiding some of the best and some of the worst days? ”

In the real world, of course, no one is able to sidestep all the good or all the bad days. But what if that were possible? The table below provides insight.

| 2023 return through 11/8 | Standard deviation of daily returns | |

| Buy-and-hold return | +14.1% | 0.85 |

| Sidestepping the 8 best days | -1.5% | 0.78 |

| Sidestepping the 8 worst days | +30.5% | 0.79 |

| Sidestepping the 8 best and the 8 worst days | +12.6% | 0.72 |

Notice that when you sidestep both the best and the worst days, you come close to matching the buy-and-hold return, but with measurably less risk. As a result, you beat the market on a risk-adjusted basis.

“The most volatile sessions on Wall Street tend to be bunched together in clusters. ”

But do market timers have a realistic shot at avoiding the trading sessions with either the biggest gains or the biggest losses — the most volatile trading sessions, in other words?

The surprising answer is “yes,” according to an academic study entitled “Volatility-Managed Portfolios.” It was conducted by Alan Moreira of the University of Rochester and Tyler Muir of UCLA.

I wrote about this study several months ago, so will briefly summarize its findings here. The professors found that the most volatile sessions on Wall Street tend to be bunched together in clusters. By reducing your equity exposure when volatility spikes upward, and restoring that exposure when volatility recedes, you have good odds of sidestepping many of the trading sessions with the biggest gains or the biggest losses.

As a result, according to the professors, you can beat the market on a risk-adjusted basis.

This year is a good example of how volatile sessions are often bunched together. Of the 16 trading days this year so far that are among either the best eight or worst eight, six occurred in a 14-trading-session stretch between March 3 and March 22.

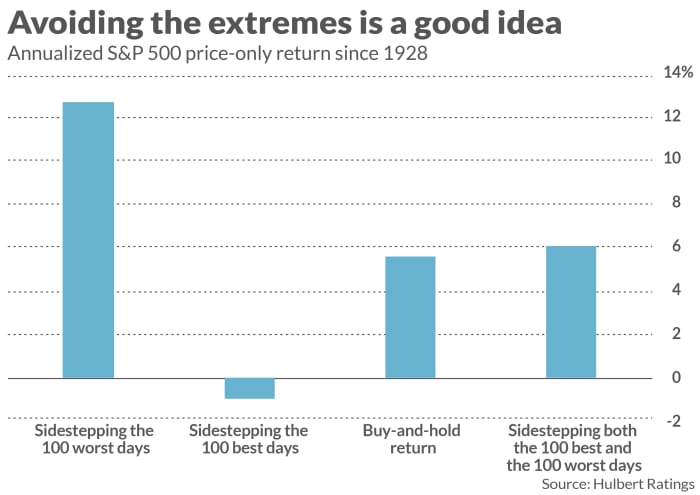

The professors document their findings with a number of statistical tests. But one simple way of appreciating what they found is provided by the accompanying chart, which focuses on all S&P 500 trading sessions since 1928.

Notice that over this longer period you actually beat a buy-and-hold strategy in raw, unadjusted terms when sidestepping both the best- and worst days. And when you take into account the risk reduction from avoiding the most volatile days, you beat the market even more on a risk-adjusted basis. That’s a winning combination.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

More: Stock-market timers beware: Just 8 days account for all of the S&P 500’s 14% gain in 2023

Plus: Stock-market rally faces make-or-break moment. How to play U.S. October inflation data.

[ad_2]

Source link

(This article is generated through the syndicated feed sources, Financetin doesn’t own any part of this article)