[ad_1]

The crisis that started two years ago, with the explosion of Covid, and continued until today, has arrived to also touch the accumulation sector.

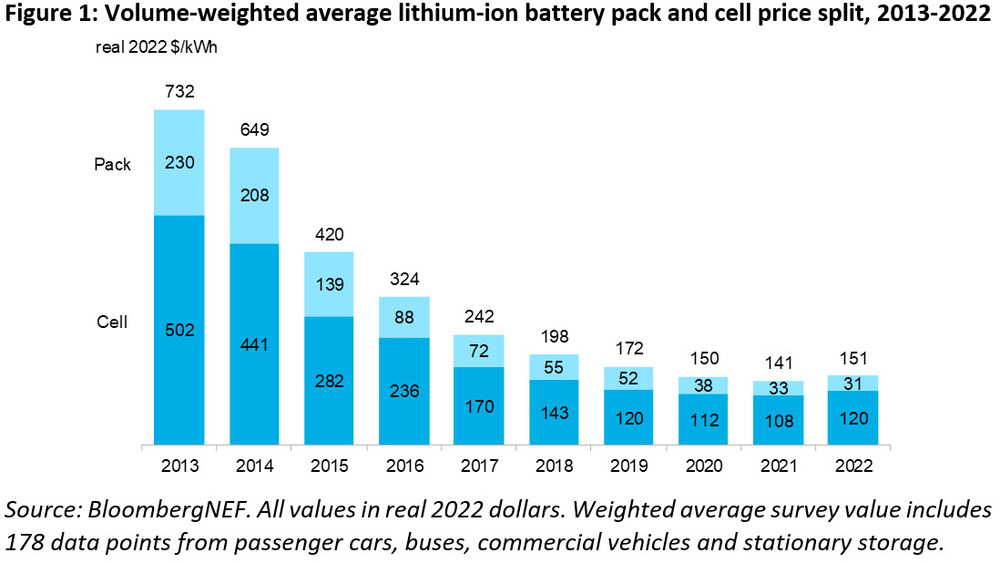

It is to report it BloombergNEF (BNEF), which has been monitoring the market since 2010, through its annual report (available here links), adding as, in ten years, there has never been any increase in the lithium-ion technology segments, including electric vehicles and stationary storage.

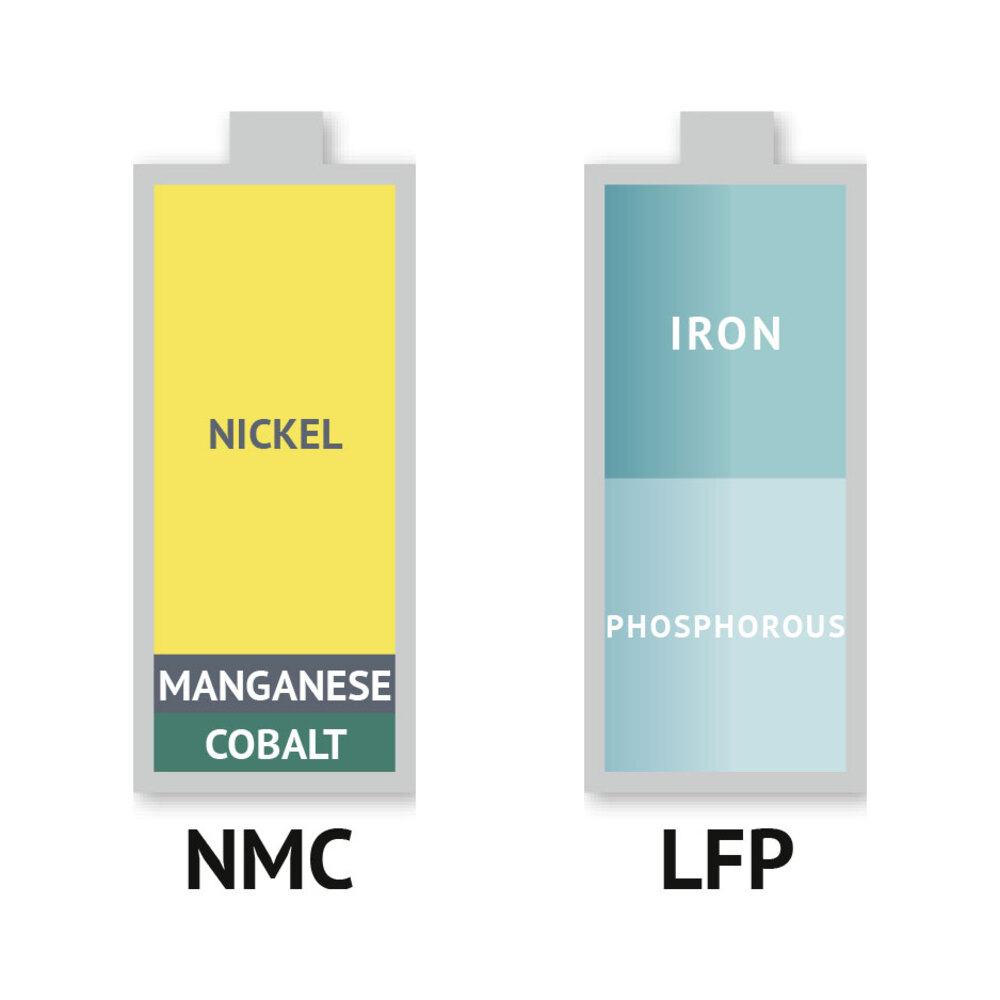

In these two sectors, the increase was held back both from the arrival of the batteries LiFePO4 (lithium – iron – phosphate), both from constant reduction of the percentage of cobalt in CMN (nickel – manganese – cobalt), which has decreased their production cost over the years.

Furthermore LFPs are on average 20% cheaper than NMCstherefore any increase must take into account the competition factor.

“Raw material and component price increases have been a major contributor to the observed cell price increase in 2022”explains Evelina Stoikou of BNEF, who went on to explain how, instead, in the automotive sector the increase was more limited “Large battery manufacturers and automakers have turned to more aggressive strategies to hedge against volatilityalso relying on direct investments in mining and refining projects”.

BNEF predicts the average battery prices they will remain high also in 2023 at about 152 $/kWhand then start over go down in 2024when new lithium mining and refining facilities are expected to support supply. “Despite a setback in falling prices, battery demand is setting new records year on year and will reach 603 GWh in 2022, double that of 2021. Growing supply at that growth rate is a real challenge for industry, but investments in the sector are also growing rapidly and technological innovation is not slowing down”. BNEF analyst Yayoi Sekine added.

.

[ad_2]

Source link