[ad_1]

Housing bears have recently ramped up their rhetoric calling for an imminent crash.

It’s not an apparently unaffordable assumption with home prices and mortgage rates nowhere near 3% anymore.

But usually, a crash or bubble occurs before any type of creative financing.

Back in 2006, it was zero down mortgages, declared income loans, option ARMs, and other very bad things.

Today, the culprit is a high-priced 30-year fixed mortgage, which is not constructive.

Home sellers can’t afford to sell now

The housing market is super weird right now. Even if homeowners want to sell, they often can’t,

Or there’s little desire due to the weird mortgage rate environment.

In short, according to the most recent HMDA data, most current home owners have mortgage rates of 5% or less. And most have 30-year fixed-rate mortgages.

Some people call these home loans “golden shackles” because they entrap the homeowners, but also provide some value.

The point is, these homeowners can’t move because you can’t take your mortgage with you (mortgage disruptors are you listening?).

Let’s consider a homeowner who bought a property in 2018 for $500,000 and then refinanced in 2021 when the 30-year rate was sub-3%.

We’ll show that his property is now valued at $700,000, and his loan amount is just over $360,000.

His monthly principal and interest payment is approximately $1,550. what a steal

Now consider that they are looking to move to a larger home to accommodate a growing family.

The asking price is $850,000 and the mortgage rate is 6.5%. If they put 20% down, a $680,000 loan amount at 6.5% costs about $4,300.

We’re talking about a 200% increase in mortgage payments. And this is not an unusual scenario.

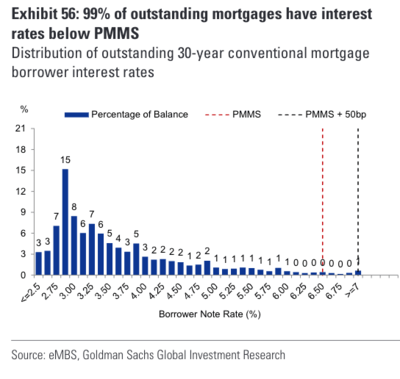

Mortgage rates for 99% of borrowers are now below market rates

A new chart is circulating from Goldman Sachs shows 99% of outstanding mortgages are priced below Freddie Mac’s weekly survey rate.

In retrospect that survey rate was 6.65%, which means almost all current homeowner mortgage rates are below that.

If you examine it closely, 28% of current owners have rates under 3%, and another 44% have rates under 4%.

This accounts for 72% of current properties, with less than 4% worth the amount. You expect them to trade for a 6.5% or 7% mortgage rate?

For the 99% of current homeowners with mortgages, there is little incentive (or desire) to move forward from a mortgage financing perspective.

Sure, some situations may require a change, and roughly 42% of homes in the US are owned free and clear (no home loan attached).

But it paints a very different housing market than the housing market we saw in 2007.

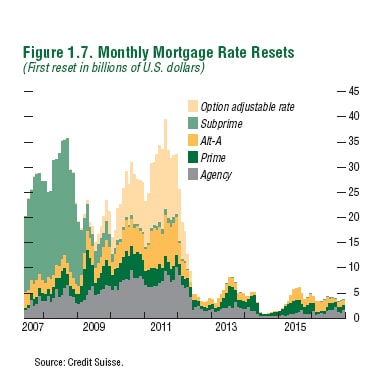

Homeowners Couldn’t Afford Living in 2007

During the Great Recession housing market, there was another chart circulating, and it looked nothing like the current chart. In fact, it was quite the opposite.

It featured hundreds of billions in adjustable-rate mortgages (ARMs) that were due to reset in the coming months and years.

By reset, I mean adjust the lot from negative amortization (or from interest only) to fully amortized payments.

Or those who were adjusting to a fully indexed rate after the initial teaser rate expired.

In any case, payments were likely to increase significantly, leading to a payment shock. And more importantly, an unaffordable mortgage.

And remember, many of these landlords were not properly qualified for the mortgage in the first place.

The options included in the chart were ARMs, subprime loans, Alt-A mortgages, and standard prime and agency equipment.

The chart was terrifying and basically summed up the volatile housing market in one simple graph. In those days, the householders were not in a position to live,

So for those of you who want to draw parallels between now and then, you can review both charts side-by-side.

Sure, home prices are up at the moment, and mortgage rates are expensive. But this is not the same housing market.

Yes, something has to give, but I don’t know if current homeowners are going to give up their sub-4% mortgage rates.

What we need for a healthy housing market are long-term stable mortgage rates in the 4-5% range.

This will be helpful for new buyers, existing homeowners relocating, and even the Feds!

[ad_2]

Source link