[ad_1]

Mortgage Rate Q&A: “Why Are Mortgage Rates Different?”

Why is the sky blue? Why are clouds white? Why won’t your neighbor cut back the branches of his tree?

These are all good questions, and questions that often puzzle even the most sensible of men.

First, let’s take a look at how mortgage rates are determined to better understand how banks and mortgage lenders come up with interest rates to begin with.

From there, you’ll need to consider why mortgage rates differ for Consumer A versus Consumer B and from lender to lender.

There is no one size fits all for mortgage rates.

- Mortgages are like snowflakes in that no two are exactly alike (well, not really)

- The subject property and the borrower will always have certain distinguishing characteristics

- This means that the risk on the underlying loan will be different and hence the interest rate will also be different.

- Lenders also price their mortgages differently, so similar scenarios can result in variable pricing.

Mortgages are complicated business, and there certainly isn’t a one-size-fits-all approach in this industry.

First, there are thousands of different banks, lenders and credit unions that offer home loans, some of them completely unique and proprietary.

These companies compete with each other to provide the lowest rates and/or the best customer service.

Well-known names may offer higher rates in exchange for their perceived trust and familiarity.

Meanwhile, the smaller ones may offer rock-bottom rates to stay in contention with the bigger players.

A larger advertising budget may mean higher rates to cover those costs. Whereas a discount lender may be able to pass along the savings if they go ultra-lean.

Additionally, every loan scenario is different (just like a snowflake), and must be priced accordingly to factor in mortgage default risk (risk-based pricing).

Simply put, the higher the risk of default, the higher the mortgage rate. But that is only the tip of the iceberg.

There are also promotional rates, such as mortgage rates that end in .99%, and innovative marketing products such as UWM’s Exact Rate that offer brokers odd rate combinations including 2.541% or 2.873%.

So these days the possibilities are truly endless when it comes to different mortgage rates.

Mortgage rates vary based on loan criteria

- Mortgage lenders make a lot of assumptions about advertised rates.

- Your particular loan scenario may be quite different from their hypothetical loan

- If it doesn’t fit inside that box, you’ll need to take into account the many pricing adjustments that apply to your mortgage.

- These adjustments have the potential to raise or lower your interest rate drastically.

Mortgage rates do not exist in a bubble – the parts affect the whole.

Banks and lenders start with a base interest rate (flat rate) and then either increase or decrease it (rarely) depending on the home loan criteria.

There are loan pricing adjustments for all types of goods, including:

Loan Amount (Conformal or Jumbo)

Documentation (complete, alleged, etc.)

· credit score

Business (Primary, Leisure, Investment)

Loan Purpose (Purchase or Refinance)

debt-to-income ratio

Property type (single-family home, condo, multi-unit)

Loan-to-Value / Combined Loan-to-Value

The more you “move on,” the higher your mortgage rate will be. and vice versa.

In short, an individual purchasing a single-family home with a conforming loan amount, a 20% down payment, and an 800 FICO score will likely qualify for one of the lowest mortgage rates available.

In contrast, a person requesting cash on a four-unit investment property with a 640 FICO score would be subject to a much higher rate, assuming they even qualify.

I’ve already covered some related topics, including why mortgage rates are higher for condos and investment properties.

Mortgage rates are also higher on jumbo loan and refinance transactions, especially cash-out ones.

And again, even with similar features, rates will differ from lender to lender, so it’s a multi-layered situation.

Advertised mortgage rates are the best case scenario

- Mortgage Rates on TV and Online Are Usually the Best Conditions

- They Intend To Be Super Attractive To Lure You In And Hold Your Business

- When the dust settles, your interest rate may not look like what you saw advertised

- That’s why it’s important to shop around and better understand how risky your particular loan is.

You know those mortgage rates you see on TV or the Internet?

They assume that you have an owner-occupied single family home, a perfect credit score, a large down payment and a commensurate loan amount.

Not to mention a newborn Golden Retriever with an unmatched pedigree.

Most people don’t have all of those things, and as a result, they’ll see different mortgage rates. And by “different,” I basically mean higher.

How much more depends on all the factors listed above. So take the advertised rates you see with a big grain of salt.

Also, take the time to shop around your home loan with different lenders and better understand your risk appetite in the process.

Find out what lenders are doing to you and take steps to fix those things if you want to get the lowest rates available.

tip: Determine if you can structure your loan slightly differently to get better pricing. This may mean a higher down payment or a different loan program, such as FHA versus conventional.

The same exact mortgage can be priced differently with two lenders

Now let’s assume that you and any other borrower have the same exact loan scenario.

You’re both down 20% on the purchase of the single-family home you want to occupy. You both have 800 FICO scores. You both want a 30 year fixed mortgage.

Heck, you’re both paying a discount point at closing to get a slightly lower interest rate. And just for fun, the lender fees are the same too.

But somehow, one lender is charging .50% higher interest rate than the other. how can that be?

Well, like any other business, it’s good old fashioned marketing.

When you go to the grocery store, you can compare two similar products. Apart from the packaging they both seem to be identical. Oh yeah, and the price.

Home loans cannot be any different. At the end of the day, you’re still getting a 30-year fixed mortgage with the same exact rate and closing costs.

The difference can only be of process and customer service. But what’s more important, the process or the monthly payments for the next 30 years?

A recent analysis by the Consumer Financial Protection Bureau (CFPB) found that price spreads for mortgages are often 50% of the APR.

So it would not be unusual to see one lender advertising an APR of 6%, while another offers 6.5%. for the same exact loan.

In other words, regardless of your credit scenario, loan type, FICO score, etc., the choice of lender matters a lot.

You may not be able to control your credit score or down payment, but you do have the ability to shop around and get multiple quotes. And it can make a real difference!

Do mortgage rates vary by state?

- Yes they definitely can! You May Get a Lower Rate in California Versus Nebraska

- Depending on the lender’s appetite for a certain geographic area

- Rates may vary from state to state, or even within certain counties

- Make sure the lender you use offers the best price for the state you live in.

one last thing. I’ve Been Asked If Mortgage Rates Can Vary From State To State, And The Answer Is Actually Yes, In fact, they may even vary by county in some cases.

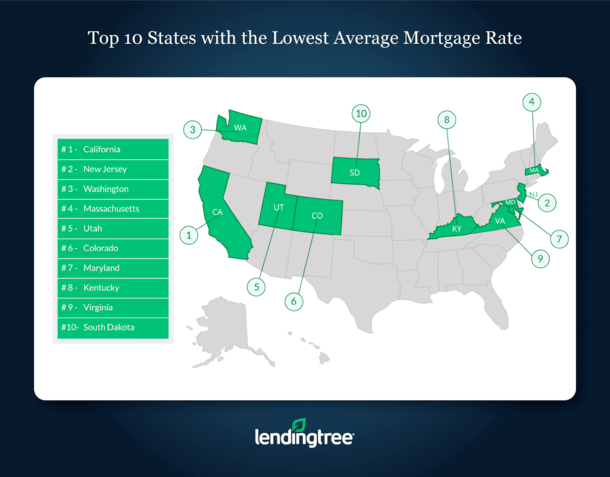

As you can see from the image below, some states have lower average mortgage rates for one reason or another.

This list is from February 2019, when the average fixed rate for 30 years was 4.84% per LendingTree across the country.

While no state offered an average rate below 4.74% or above 4.96% (a fairly narrow range), there was some variation based on locality.

California led the nation with an average rate of 4.74%, followed by New Jersey, which saw an average of 4.75%, and Washington and Massachusetts both averaged 4.76%.

Nothing spectacular, but different nonetheless.

But it may not be due to any one reason, such as a higher default rate in state X or fewer natural disasters in state Y. Or more rules in any other state.

It may have more to do with the fact that lenders are looking to grow their business in a certain part of the country, and thus they will offer some kind of pricing special or incentive to drive down rates in California.

That’s why you may see a rate sheet that says .50% discount state adjustment for loans in CA and FL, for example. This will give them a competitive advantage in those areas.

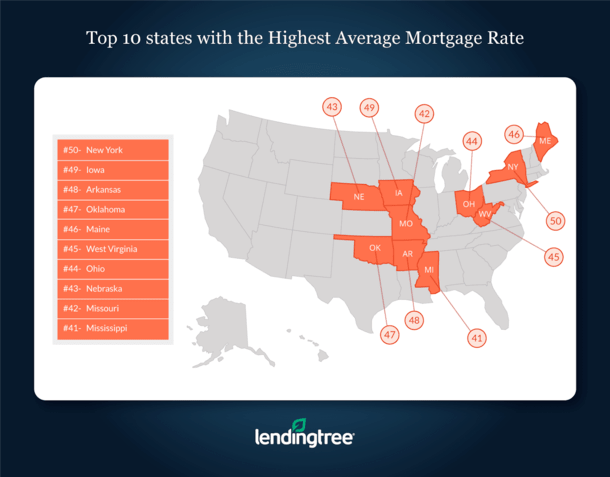

How about states where mortgage rates are slightly higher, such as New York, Iowa, and Arkansas, which average 4.96%, 4.93%, and 4.92%, respectively?

It is possible that you could see a pricing adjustment of .25% for one of these states which could raise the interest rate somewhat.

In other words, the rates can be both higher or lower depending on the state where the property is located.

Of course, if this results in unfavorable pricing, you can simply move to a different lender that doesn’t charge as much for the state.

All the more reason to shop around, compare mortgage rates online, and talk to a mortgage broker or two.

Once you’ve done that, check mortgage rates with your local bank or credit union as well.

Don’t be one of the many people who only get a mortgage quote because you may be paying too much.

Read more: What Mortgage Rate Can I Expect?

[ad_2]

Source link