[ad_1]

The housing market has been extremely disappointing for potential home buyers.

Not only have mortgage rates doubled over the past year, but home prices remain extremely high despite some minor improvements.

Sure, you may hear that the housing market is crashing, or that we’re having a home price correction.

But it doesn’t mean much when you zoom out and look at home prices over the years.

Worse still, despite the extremely low affordability, home prices may not even come down.

Home prices are up 5.3% from a year ago

While some overheated metros have declined across the country, home prices up 5.3% Nationwide from January 2022 to January 2023.

This is according to the latest seasonally adjusted monthly House Price Index (HPI) by the Federal Housing Finance Agency (FHFA).

They rose 0.2% in January from a month earlier after registering a 0.1% monthly price decline in December 2022.

If we drill down a bit deeper, seasonally adjusted monthly home prices from December 2022 to January 2023 showed a wide range, looking at nine census divisions.

Home prices were up 0.6% in the Pacific Division and 2.0% in the New England Division.

On a trailing 12-month basis, prices were up -1.5% in the Pacific and +9.6% in the South Atlantic division.

as i always say, real estate is localAnd this is especially true these days when some markets are in different phases than others.

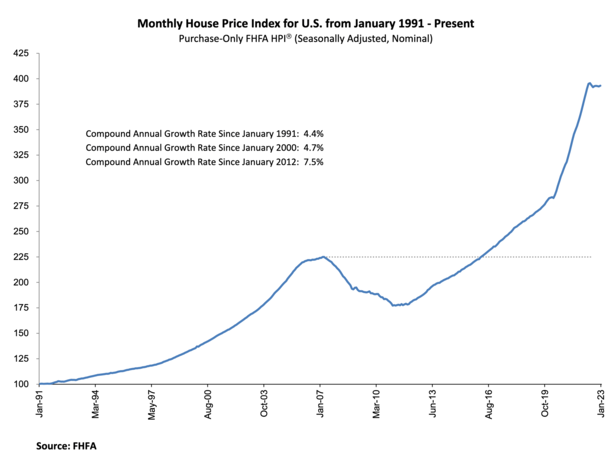

But look at the national home price chart above. Home prices have absolutely gone up in the last few years.

And they pulled back a small amount before flattening out. The takeaway is that house prices are high and cannot go down much.

Home prices haven’t fallen much as inventories remain tight

Despite fake home prices and questionable, speculative purchases from investors, home prices have held up fairly well.

If you’re looking at that home price chart and wondering how on earth prices could be above the levels seen in 2006-2008, blame inventory,

There has been a severe shortage of homes for sale for several years, exacerbated by the mortgage rate lock-in effect.

In short, many of today’s homeowners have 30-year fixed-rate mortgages that cost between 2-4%.

Also called the Golden Shackles (assuming they want to sell/relocate), these low rates make it very difficult to part with the property.

Even if they are able to buy a home later, they may be locked out of the new interest rate set at 6%.

This explains why the number of existing unsold homes stood at just 980,000 at the end of February. National Association of Realtors,

That’s just 2.6 months of supply at the current monthly sales pace. And as we know from supply and demand, when supply is low and demand is high, the price goes up.

For the record, the median existing-home price fell 0.2% to $363,000 in February, ending 131 months of year-over-year increases, the longest in history.

So there is some pressure on house prices, but 0.2%? Isn’t it going to do a lot?

How much income is needed to buy a home today?

The rule of thumb for housing costs is approximately 28% of your gross income. So if you make $80,000, no more than $1,867 can go toward the mortgage.

This includes principal and interest, property taxes, home owner’s insurance, and PMI and HOA dues, if applicable.

The problem is that the median home value in the United States is $327,514 ZillowAnd 6.8% higher than the previous year.

US real median household income Was $70,784 in 2021, and has actually declined since 2019 due to inflation.

If we consider buying a $325,000 home with a 20% down payment, we arrive at a loan amount of $260,000.

We’ll throw in a 6% mortgage rate to arrive at a P&I payment of $1,558.83. Now add taxes of $340 per month and home owners insurance of $100 per month.

That puts us at roughly $2,000 a month, or about 34% of that $70,784 median income.

That’s not terrible, but it’s still well above the 28% rule for housing payments. And that’s using optimized math.

If it’s a 5% or 10% down payment, you’ll have a higher PMI, a higher mortgage rate, and a larger loan amount.

so it’s pretty clear house prices are unaffordable For the most part at their current levels. But without meaningful additions to inventory, things won’t change.

And as mentioned, many of the current owners aren’t going anywhere. The only games in town are newly built houses, but builders can only build so many.

Additionally, new construction is often not located in densely populated areas where there is a greater need for new, affordable housing.

In California, only 21% of all residents will earn the minimum income needed to buy a home in 2022 with a median price of $822,320, down from 27% in 2021. car,

It was slightly better nationwide, with 43% able to afford a property worth an average of $392,800.

What happens next for house prices?

black Knight noted Home prices rose 0.16% in February after seven consecutive monthly declines.

It was the strongest one-month gain since May 2022, although at 1.94%, annual home price growth fell below 2% for the first time since 2012.

This supports the thesis that home price growth was about to slow down, aka Low year-over-year home price growth,

But that real, falling home prices will still be difficult. And now that we’re entering home buying season in the spring, home prices may actually be on the rise again.

Mortgage rates are also declining, hovering around their 30-year February low of 6.125%.

Rates were about 1% higher in early March, so there could be some serious headwinds for the housing market, at least in terms of home price trajectories.

Sadly, this means that even those with an average income will find it difficult to buy a home. And even though home prices are very high, they may remain that way for the foreseeable future.

Ultimately, we may face years of relatively flat home price growth, which will still put home ownership out of reach for many people.

Of course, there are affordability solutions coming to market, whether it’s the California Dream for All loan, or the floating rate buydown.

For those anticipating or anticipating a housing crash, you need to look at the basics. It’s not 2008, even though home prices are much higher.

Mortgages are very different and housing is in very short supply. Until that changes, it will be difficult to draw too many parallels.

[ad_2]

Source link