[ad_1]

This year’s strong rally has stuttered over the past few weeks. August has generally seen increased volatility and declines in the main market indexes. But that hasn’t affected a basic truth of the financial markets: stocks are individuals, and they rise and fall for idiosyncratic reasons. Investors should always check under the hood, to find out if a bargain price represents a good buy.

That check can be rough, however, as there are reams of data to sort. Fortunately, investors can always turn to the Smart Score, an AI-powered data collection and collation tool, based on the TipRanks database, that rates every stock according to a set of factors proven by history to match up with future outperformance. Look for stocks that combine the highest Smart Score, a ‘Perfect 10,’ with a pullback in share price – that’s where the true bargains may be hiding.

We can get started with a look at two Strong Buy stocks that feature both reduced share prices and a ‘Perfect 10’ from the Smart Score. These are stocks that have attracted analyst attention; are they right for you?

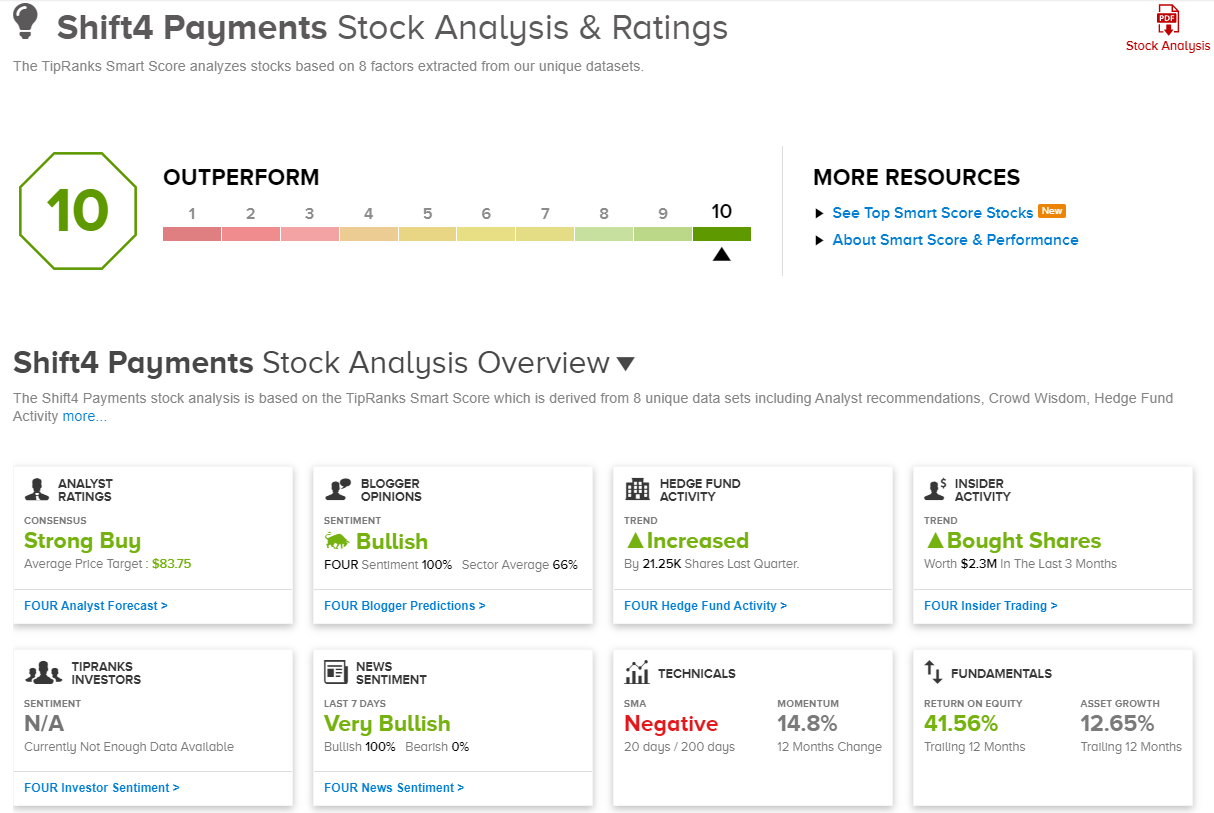

Shift4 Payments (FOUR)

The first ‘Perfect 10’ stock on our list is Shift4 Payments, a tech firm working in the payment processing business. The Allentown, Pennsylvania-based firm provides services across a wide range of industries, and counts some big names among its customer base: Best Western Hotels, Applebee’s, the Utah Jazz, Gold’s Gym. Overall, the company boasts more than 200,000 customers and over 7,000 sales partners, and processes more than 3.5 billion transactions worth more than $200 billion annually.

In an important announcement, earlier this month Shift4 indicated that it is nearing the closure of its Finaro acquisition. The $525 million move will give Shift4 access to Finaro’s European processing network. The deal was expected to have closed in March of this year, but was held up due to ‘regulatory requirements;’ it is now expected to close in Q3/early Q4.

The company reported its 2Q23 results early this month, and showed a series of gains, including year-over-year revenue and earnings growth, that beat expectations. At the top line, the company reported revenues of $637 million, up 26% year-over-year and almost $4 million better than had been anticipated. The bottom line figure, a non-GAAP adjusted EPS of 74 cents per share, was 22 cents ahead of the estimates, and more than triple the year-ago result. The company saw a 59% y/y increase in end-to-end payment volume, and a 61% y/y increase in gross profit.

Despite the strong results, the stock has been through a bit of a selloff recently, having retreated by 19% during August. For Raymond James analyst John Davis, the stock’s price decline makes it an attractive bargain buy. He writes in his coverage, “We see upside to FY24 Street estimates, assuming Finaro does in fact close, given the Street is implying just ~22% organic revenue growth (~800 bp decel) and ~80 bp of EBITDA margin expansion… The stock is now trading near trough valuation levels at just 10x FY24E EBITDA and a ~20% discount to the S&P 500 on EV/EBITDA. As such, we view the recent weakness as a compelling entry point and recommend investors initiate or add to positions.”

As such, Davis recently upgraded his stance on FOUR, bumping it from Neutral to Outperform (a Buy). The analyst complements his new rating with a $74 price target, implying a one-year upside potential of 33% from current levels. (To watch Davis’s track record, click here.)

Shift4 has picked up 17 recent analyst reviews, including 16 to Buy against just 1 to Hold, to back up its Strong Buy consensus rating. The shares are trading for $55.76, and the $83.75 average price target suggests it will gain 50% in the year ahead. (See Shift4 Payments’ stock forecast.)

Crocs (CROX)

Next up is Crocs, a recognizable brand name in footwear. The company built its name on its eponymous foam clogs that became such a hit in the early 2000s. Today, the company offers a wide range of footwear lines, from the foam clogs to flip flops to sandals, boots, and comfortable work shoes. The company even markets a line of shoes designed for healthcare professionals who spend long days on their feet.

By the numbers, Crocs has built itself an empire. The company has sold more than 850 million pairs of shoes since it hit the markets in 2002. Crocs employs over 5,900 people and has a presence in 85 countries around the world, and makes over 2 billion sales annually. Together, all of this puts Crocs among the world’s top ten athletic footwear brands.

Earlier this summer, Crocs reported its 2Q23 financial numbers – and showed a record revenue figure of $1.072 billion. This was up 11% y/y, and was $29.2 million ahead of the forecast. At the bottom line, Crocs reported earnings of $3.59 per share by non-GAAP measures. This marked an 87-cent per share increase over the prior year’s Q2 earnings, and was 61 cents per share better than expected.

However, investors did not like the outlook. For Q3, the company sees adj. earnings hitting the range between $3.07 to $3.15 per share, at the midpoint, below consensus at $3.12. Moreover, with Q3 revenues expected to grow around 3% to 5% y/y, there are concerns about slowing growth. The result is a stock that has been on the backfoot since the Q2 print, down by 21%.

Nevertheless, Jim Duffy, 5-star analyst from Stifel, takes an upbeat view of CROX, basing his stance on net positives from the earnings results and on the company’s brand strength, writing, “FY2Q results were a mixed bag but positives outweigh the negative and the [pullback] in shares presents an opportunity. Market disappointment reflects the shortfall from HEYDUDE wholesale (~15% of global revenue) but looks past positive developments for the Crocs brand (~75% of global revenue). Specific factors showcasing improved balance and increasing our confidence into FY24 include 1) Crocs N. America brand strength and product diversification, 2) Crocs international strength led by +40% DTC comp and Asia/China, and 3) debt reduction bringing net leverage <1.7X.”

Duffy goes on to point out that Crocs has a solid foundation for future gains: “Profit pool diversification, improved balance sheet optionality, and a very forgiving valuation increase our confidence in risk adjusted return prospects for CROX shares.”

At bottom, all of this supports Duffy’s Buy rating, while his target price of $130 points toward a 36% gain on the one-year time horizon. (To watch Duffy’s track record, click here.)

Of the 9 recent analyst reviews on CROX, 7 are to Buy and 2 to Hold, enough to bring in a Strong Buy consensus rating. The stock’s $95.56 share price and $152.75 average price target suggest a robust 60% upside over the next 12 months. (See Crocs’ stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

[ad_2]

Source link

(This article is generated through the syndicated feed sources, Financetin doesn’t own any part of this article)