Option Greeks are financial measures of the sensitivity of option prices to important determinants such as volatility or the price of the underlying asset. In Greek, option portfolio analysis and sentiment analysis of options or groups of options. Many traders believe that options trading requires informed decisions. Delta, Gamma, Vega, Theta, and Rho are the most important choices for Greeks. However, there are many other Option Greeks that can be derived from those listed above.

Option Greek Delta?

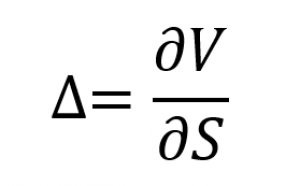

Delta (Δ) measures the sensitivity of the change in the price of the option to changes in the price of the underlying asset. In other words, if the price of the underlying asset increases by $1, the price of the option will change by Δ. Mathematically, the delta formula is

Where:

∂ is the first derivative

V – Option price (theoretical)

S – price of the base asset

Note that we take the original derivative of the option and the price of the underlying asset because the derivative is a measure of the change in the interest rates of the variable over a period of time.

Delta is usually calculated as a decimal number between -1 and 1. A call option’s delta can be between 0 and 1, and a put option’s delta can be between -1 and 0. The closer the option’s delta is to 1 or -1, the deeper the option. The delta of an option portfolio is the weighted average of the deltas of all options in the portfolio. For At the money option Delta is 0.5.

Delta is also known as the hedge ratio. If a trader knows the delta value of an option, he can hedge the position by multiplying the delta by the amount of the underlying asset bought or sold.

Gamma

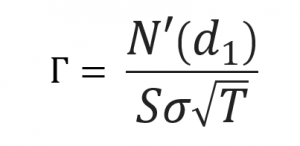

Gamma (Γ) is a measure of the change in delta relative to changes in the price of the underlying asset. If the price of the underlying asset increases by $1, the option’s delta changes by gamma. The most important use of gamma is to estimate the delta of an option.

Gamma formula

Where,

N(d1) = delta

T = time to maturity

q = Sigma

S = Price of underlying

Long options (both call and put) have positive gamma. At the Money options have largest gamma (the strike price of the option contract is equal to the price of the underlying asset). However, when the option declines or runs out of money, the value of gamma decreases.

Option Greek: Vega

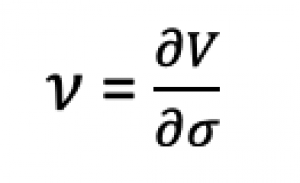

Vega (ν) is a Greek option that measures the sensitivity of the option to the volatility of the underlying asset. If the volatility of the underlying valuation increases by 1%, the option price will change by the amount of Vaga.

Vega formula

Where:

∂ is the first derivative

V – Option price (theoretical)

σ – the volatility of the underlying asset

Vega is expressed as a sum, not a decimal. An increase in vega usually corresponds to an increase in the value of the option (Both Call and put).

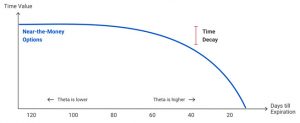

Theta

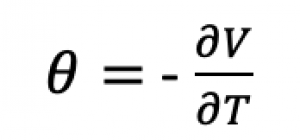

Theta (θ) is a measure of option price sensitivity to expiration. If the option expires by 1 day, the option price changes by theta. Theta option greek is also called time Time decay. theta formula

Where:

∂ is the first derivative

V – Option price (theoretical)

τ – time to maturity

In most cases, theta is negative for options. However, this could benefit some European opportunities. Theta is decay much faster near the expiry of option hence most of the traders place the trades near the expiry for less cost and high profit.

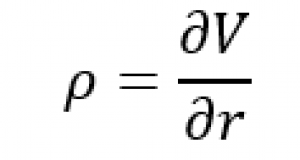

Rho:

Rho measures the sensitivity of option prices to interest rates. If the base rate increases by 1%, the option price will change the Rho amount. Rho is considered the smallest of the other Option Greeks because option prices are generally less sensitive to changes in interest rates than to changes in other parameters. Rho formula

Where:

∂ is the first derivative

V – Option price (theoretical)

r – interest rate

In general, call options have a positive rho and call options have a negative rho.

You can use and download the following excel workbook for calculating option Greeks by yourself.

Click here to download your excel calculator for options